Investor sentiment one year on from Russia-Ukraine invasion

Professor Eliza Wu

Geopolitical instability has escalated around the world following Russia’s unlawful decision to launch a full-scale military attack on its neighbour Ukraine on 24 February 2022.

The human toll has been devastating with the loss of well over 40,000 innocent lives and a large displacement of families and the fleeing of refugees young and old.

Western states have been sending military weapons to aid Ukraine’s defence and using jawboning and imposing non-military interventions in the hope of a ceasefire.

Yet, in spite of the economic and financial sanctions imposed to hurt Russia’s economy and its access to the rest of the world resulting in major changes in trade flows, the war continues, and investor confidence in the region plummets.

One year on from Russia’s first strike on Ukraine, we assess how global investor sentiment and the world economy have changed. What are financial markets likely to do from here with no resolution in sight?

Investor sentiment

Investor sentiment encompasses the emotions and attitudes of investors regarding both the economy and their investments. It can have a significant impact on financial markets, prices, and produce volatility in investments in financial assets like equities and fixed-income securities.

Financial markets comprise two broad categories of investors: retail and institutional.

Retail investors are those who invest their own funds in financial markets and generally manage smaller investment portfolios. Conversely, institutional investors are organisations that invest massive amounts of capital on behalf of others.

Given their enormous investment capacity, institutional investors possess significant sway over financial markets. However, retail investors also wield influence in the short term, especially in light of recent developments around their increasing reliance on social media and online trading platforms that enable them to coordinate their trading activity and influence market trends more readily than ever before.

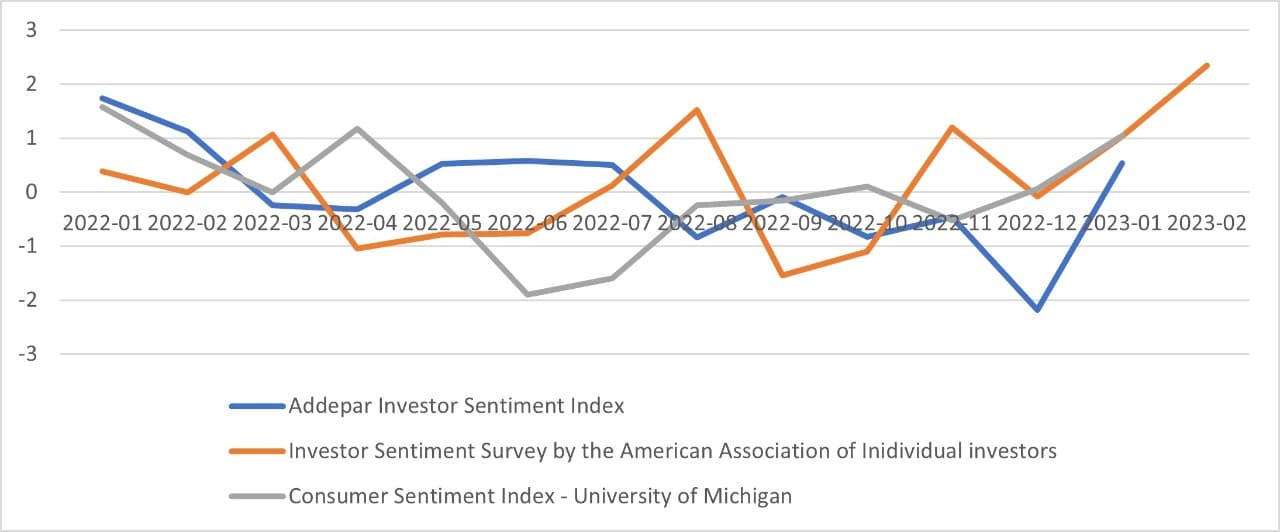

Figure 1: Investor sentiment. Sources: Addepar, the American Association of individual investors, University of Michigan

Understanding investor sentiment since the outbreak of the Russia-Ukraine war is crucial to comprehending the fluctuations in financial markets. We resort to leading industry investor sentiment indexes to make sense of investor sentiment.

All three indexes, be it for the entire market or individual investors, indicate that investors experienced profound fear and pessimism in February and March of 2022 when the war first began, with the onset speed and brutality of the conflict catching many off guard.

The outlook for 2023 remains decidedly bearish, particularly in the first half of the year. However, after a year of ongoing geopolitical uncertainty, investors seem to have come to terms with the ongoing geopolitical tension and uncertainties brought on by Russia, with sentiment improving in all three indexes.

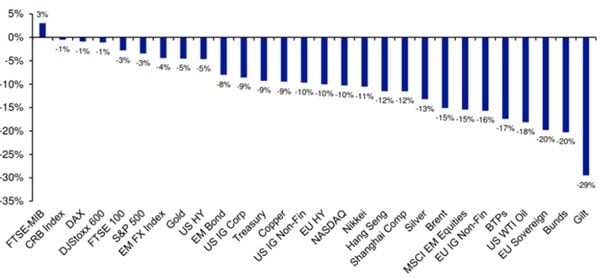

Figure 2: One-year performance of major asset classes. Sources: BLOOMBERG FINANCE LP, DEUTSCHE BANK, Marketwatch

The Russia-Ukraine conflict brought an immediate end to the era of ultra-low interest rates and triggered steep hikes in energy prices. The sharp increase in gas and oil prices also rapidly spilled over into other commodities, such as copper, aluminium, and nickel. Inflation has skyrocketed globally, with consumers grappling with the soaring costs of living right around the world.

Governments and central banks, including those in Australia, have been compelled to pivot urgently towards fiscal and monetary policies that focus on tax adjustments and interest rate hikes that combat inflation.

The bearish investor sentiment is palpable across the world’s major financial assets, with equity markets in developing nations and the US experiencing the most significant decline (see Figure 2).

In contrast and perhaps somewhat counterintuitively, the main European share markets have proven more resilient to the geopolitical turbulence in the region, despite being in much closer proximity to the conflict than other parts of the world. For instance, the German DAX has fallen by one percent and the FTSE by three percent.

Following several wild swings, oil, gas, and other commodity prices have settled down (see Figure 3). However, the issue of energy security remains a continuing concern for Europe.

Germany and Europe, more generally, have managed relatively well in the past year to reduce their dependence on Russia for their high energy needs. They have done this by diversifying energy infrastructure away from Russian oil and gas, but the significant energy shock has driven energy prices sky-high and fuelled inflationary pressures in all corners of the world.

Global inflationary pressures and real economic impacts

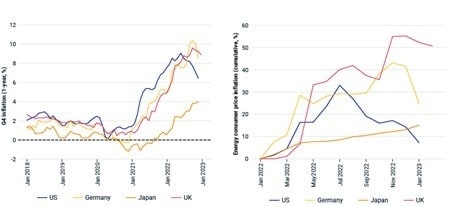

Figure 3: inflation and energy prices. Source: MSC

The Russian-Ukrainian conflict has adversely impacted the global economy, significantly disrupting production and trade, while escalating food and energy prices. This has led to high inflationary pressures in major economies like the United States, Germany, Japan, and the United Kingdom (see Figure 3).

The Ukrainian economy has been completely decimated and economic growth within the Russian economy has also suffered a debilitating nose-dive (see Figure 4).

It is undeniable that the war has had a devastating impact on both the Russian and Ukrainian local economies and their respective national infrastructure, resulting in a lose-lose situation for both nations. The significant decline in real GDP growth for both countries is a stark indicator of the economic damage wrought by the conflict.

The National Bank of Ukraine has reported a year-on-year contraction of 26.6 percent in its economy and an unemployment rate of 26 percent, underscoring the extent of the war and crisis. Migration outflows and high unemployment levels will scar the region for many years to come.

Conclusion

Figure 4: Russian and Ukraine annual real GDP growth. Source: Committee for the Abolition of Illegitimate Debt

Global investor sentiment has been hit hard by the deteriorated geopolitical situation emanating out of Europe. Global availability and pricing of energy and food has been significantly impacted by the war.

The economic costs of Russia’s invasion of Ukraine have been felt across the globe, but the adverse impact on the Russian-Ukrainian region has been particularly devastating on local citizens facing infrastructure damage, high inflation, unemployment, migration outflows, and structural changes that have altered their future livelihoods for the worse.

The world is a different place one year on and significant risks remain for the global economy and for the stability of world order. Ending Russia’s unlawful invasion of Ukraine is a top-order priority for governments of all political orientation – warfare kills too many innocent lives, inevitably induces bearish market sentiments, and harms economic stability and prosperity.

A year on from the war, investors have acclimated to the persistent geopolitical ambiguities of the war and have momentarily tranquilised market concerns. A resurgence in investor sentiment is probable only in the event of a significant turning point in the conflict.

Should the war continue its current protracted trajectory, investor sentiment is unlikely to experience significant fluctuations – just similar to the frog in the pan.

This article was first published by the Australian Institute of International Affairs as 'Political Conflict and Investor Sentiment Around the World: Russia-Ukraine One Year On'.

Professor Eliza Wu is Head of the Discipline of Finance at the University of Sydney Business School. Associate Professor Angel Zhong is an award-winning RMIT finance researcher.

Related articles

Home buyers likely to be happier retirees