Academics call for balanced regulation for buy now, pay later schemes

University of Sydney Business School academics from the Discipline of Business Analytics, Honorary Associates John Watkins and David Grafton, and Associate Professor Andrew Grant from the Discipline of Finance have submitted a detailed response to the Australian Government Department of Treasury’s Consultation on Buy Now, Pay Later (BNPL) Regulation.

The Treasury Options Paper outlined eight areas of regulatory issues, including unaffordable lending practices and non-participation in credit reporting. Academics responded to each utilising data-driven insight from their recent research Buy Now Pay Later: Multiple Accounts and the Credit System in Australia – the highlights of which are included in this media release Buy Now Pay Later regulation needed to protect vulnerable borrowers.

The academics utilised transaction data from over 800,000 consumers for the study, identifying BNPL users and their key characteristics. The authors acknowledge that the majority of consumers use BNPL safely, finding 77% of consumers who used BNPL were in low or very-low risk grades. Despite the benefits to many, the innovations revealed weaknesses in the Australian credit regulatory framework that put a vulnerable group of consumers at greater risk from forms of credit beyond just BNPL.

Three observations of note that were shared with the Treasury.

Study shows unaffordable lending practices lead to debt stacking

The study found evidence that those showing signs of financial risk were more likely to hold multiple BNPL accounts.

The likelihood of holding multiple BNPL increases:

- 2.2 times if in the highest risk of missing payments in next 12 months,

- 2.1 times if recently maxed out on a credit card,

- 1.7 times if holding a personal loan,

- 1.5 times if in the lowest socioeconomic group, and,

- 1.3 times if receiving government benefits.

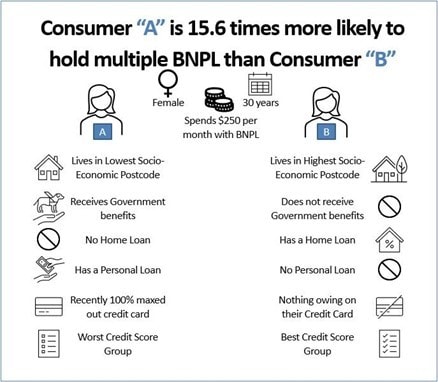

The diagram below showcases the increase in likelihood to stack debt in vulnerable groups by holding multiple BNPL accounts, comparing the maximum risk to minimum risk consumer.

Image: Example of consumers with debt stacking risk on vs risk off

The authors’ response submission outlined that increasing transparency by providing BNPL data to one or more credit reporting bodies (CRBs) is the single most powerful way to address most issues raised in the Treasury’s regulatory options paper.

Greater transparency of BNPL holdings will ensure that financial abuse, affordability assessments, debt stacking, and other concerns are more readily identified and able to be addressed throughout the credit life cycle.

Beyond BNPL credit products, the current regulation for credit in Australia has several loopholes that mean balance information, powerful to protect the vulnerable, is not shared by any lenders, and lenders who are not the ‘Big Four’ banks have no obligation to share comprehensive credit reporting information.

Debt balance data needed at credit reporting bodies (CRBs)

The current comprehensive credit reporting legislation does not allow for balance outstanding on lending products to be shared with CRBs – an inconsistency with international standards.

This information is critical to support both affordability and credit assessment, to prevent overextending credit to vulnerable consumers. The University of Sydney study identified that:

- Consumers recently maxed out on their credit cards are 2.1 times more likely to hold multiple BNPL accounts (debt stacking),

- BNPL users with credit cards with utilisation rates above 40 percent are more likely to hold more than one BNPL account, and

- Holding a revolving credit card balance is strongly predictive of holding multiple BNPL accounts.

This indicates consumers are turning to BNPL, often multiple accounts, when other available avenues of debt are exhausted – potentially deepening their financial difficulties. This is only identifiable when account holding and balance information is available at CRBs.

Broader participation in sharing information with the CRBs needed

The current mandatory participation threshold is for Australian Credit License (ACL) holders with over $100 billion in assets (lending balances).

This limits mandatory participation in CRBs to the Big Four banks in Australia, and only mortgage lending can reach the $100 billion threshold.

The entire credit card market outstanding balances in Australia is $39 billion as at October 2022.

These gaps in the completeness of participation in credit reporting can lead to the following consumer harms:

- Non-prime lending, where most consumer harm can occur, is not transparent for lenders to make affordability and credit assessments.

- Consumers do not benefit from an improved credit rating from good repayment behaviour. This is especially important for younger consumers who are primary users of BNPL.

- Financial abuse and consumer scams are more likely to go unnoticed when there is no mandatory reporting for ACL holders outside of the $100 billion in assets threshold.

- Some lenders only report to a subset of CRBs (for example, illion has a large dataset of non-traditional lenders). Credit providers may obtain incomplete information if they only search on a single credit bureau when participation is not mandatory.

The authors will continue to engage with the Australian Government Department of Treasury for any further questions on their response to the consultation.

In addition, these University of Sydney Business School academics continue their research into which Australians are doing better, worse, or the same with the introduction of BNPL. Their balanced and independent approach recognises the benefits of this product that are safely enjoyed by millions of Australians, and aims to continue to explore who is impacted and how to shape protection for the vulnerable without impacting the benefits.

Explore Business Analytics at the University of Sydney Business School.